MONTHLY BLOGS

What You Can Negotiate When Buying a Home in Canada (That Most Buyers Don't Realize) [July 2026]

When most people picture negotiating on a home, they picture one number: the list price. You offer somewhere under the asking price, the seller counters, you settle in the middle, and whoever gives up the most ground "loses." For a lot of buyers, that back-and-forth over the sale price is the negotiation.

It's only a fraction of it. The price is the headline. The real negotiation happens in the terms underneath it, and in 2026 those terms matter more than they have in years. The market has rebalanced: nationally, inventory sat at about 5.2 months at the end of April, close to its long-term average and squarely in balanced territory, which means neither side holds the kind of leverage sellers had a few years ago.¹ For buyers, that's real room to negotiate that simply wasn't there during the bidding-war years.

So here's what actually separates the buyers who come out ahead. It isn't the ones who push hardest on the price. It's the ones who understand everything that's on the table, and know which things are worth asking for.

The Price-Only Trap

It's easy to assume a seller cares about one thing: the highest possible number. In practice, most care about more than that. They care about certainty, meaning whether the deal will actually close. They care about timing. They care about whether your financing will come together, or fall apart partway through.That matters for you, because it means you have more to work with than a single figure. A buyer who treats the offer as a package price, terms, timing, and conditions all together can often create a better outcome than a buyer who just hammers on price. That's why a clean, well-structured offer can beat a higher one: to the right seller, the certainty is worth more than the extra dollars.

So before you anchor on a number, widen the lens. Here's what else is on the table.

The Money Levers Beyond the Price

Some of the most valuable things you can ask for never touch the sale price directly. They change what the deal actually costs you.Start with a seller concession. In a balanced market, sellers are more willing to give one, whether that's a straight price reduction or agreeing to cover certain costs to get the deal across the line.² It's worth asking for any time the upfront cash is your tightest constraint. (You may have read about U.S.-style rate buydowns, where a seller pays to lower your mortgage rate. They exist here but are far less common, and our five-year renewal cycle blunts the benefit, since any rate advantage resets at renewal. With five-year fixed rates already near 4%, the math rarely works the way it does south of the border.³)

The bigger money story in Canada is often on your side of the table, in the costs you can offset. Closing costs here include Land Transfer Tax, which can run into the thousands. But first-time buyers can recover meaningful rebates: up to $4,000 provincially in Ontario, with Toronto adding more on top.⁴ And tax-free tools like the First Home Savings Account let you set aside up to $40,000 toward your purchase.⁵ Knowing which of these you qualify for can outweigh a modest price cut, and it's exactly the kind of thing a good REALTOR® will walk you through.

The Inspection Is Your Second Negotiation

In Canada, a lot of the real negotiating happens through your conditions. After years of buyers waiving conditions to win bidding wars, conditional offers are making a comeback as the market rebalances.²A home-inspection condition gives you a window, usually 5 to 10 business days, to have the home professionally inspected. An inspection on almost any home turns up something worth addressing, and when it does, you have a fresh round of leverage. You can ask the seller to make the repairs, ask for a price reduction or a credit so you can handle them yourself, or, if the issue is serious enough, walk away. Pair it with a financing condition so your mortgage is fully approved before the deal goes firm.

A few rules of thumb. Focus on what genuinely matters, meaning health, safety, and the big-ticket systems like the roof, furnace, or foundation, rather than nickel-and-diming every cosmetic flaw. And treat the report as a planning tool, not just a bargaining chip. An aging furnace isn't necessarily a deal-breaker. It's a heads-up that helps you budget.

Terms and Timeline: The Wins That Aren't About Money

One of the most powerful levers costs you nothing: flexibility. To a seller, time is often worth as much as dollars.Say the sellers need a few extra weeks before they hand over the keys because their next place isn't ready. A flexible closing date, or a post-closing occupancy (a rent-back) that lets them stay on for a short period, can make your offer the one they choose. Your deposit matters too: a strong, well-structured deposit signals you're serious and your offer is solid. The closing date, the length of your conditional period, and how your deposit is framed are all things you can shape to fit what the seller needs.

The strategic move is simple. Give the seller the timeline they need, and you'll often get the terms you want in return.

What Actually Comes With the House

This is the simplest ask of all, and the one buyers most often forget to make. In Canada it comes down to two words: chattels and fixtures.Fixtures are attached to the home, like built-in shelving or light fixtures, and they generally stay unless the seller specifically excludes them. Chattels are movable, like the fridge, the washer and dryer, or the patio set, and they don't come with the home unless they're named in the Agreement of Purchase and Sale. So if you want them, ask, and get them written in. The best practice is to spell out exactly what stays, right down to the make and model for the big-ticket items, so there's no dispute on closing day.

And if there's something you love, ask for it. The worst answer you'll get is no.

How to Actually Use the Whole Menu

Knowing what's negotiable is the easy part. Using it well is what turns a list of asks into a better deal.The buyers who succeed don't fire off every possible demand at once. They lead with what the seller values most, structure their conditions and requests thoughtfully, and avoid the death-by-a-thousand-cuts approach that makes a seller dig in. Above all, they read the seller's real motivation, and that's where a sharp REALTOR® earns their keep, negotiating the price, the conditions, the chattels, and the timeline as one strategy.

A calm, well-prepared buyer with a clear strategy almost always does better than an aggressive one throwing elbows. The goal isn't to beat the seller. It's to structure a deal that works for both sides, and to make sure you're not leaving value on the table you never knew was there.

If you're getting ready to buy, this is exactly the kind of thing worth talking through before you write an offer. I'm glad to walk through everything you could be asking for in your situation. No pressure, just a clear picture so you can make a confident decision.

Sources

1. CREA — National Statistics (balanced market, April 2026)

2. RE/MAX Canada — How Conditional Offers Are Making a Comeback

3. Ratehub — Best 5-Year Fixed Mortgage Rates, Canada

4. Deeded — First-Time Home Buyer Incentives in Ontario 2026

5. Canada.ca — First Home Savings Account (FHSA)

House Hacking in 2026: What the Hype Got Wrong and What Actually Works [June 2026]

If you've spent any time on real estate social in the last few years, you've probably seen the house hacking pitch. Buy a property, rent part of it out, let your tenants cover the mortgage. Live for free. Build wealth while you sleep.

It sounds like the kind of thing that works great in a YouTube thumbnail and falls apart in real life. And honestly? Sometimes it does.

But here's what those videos usually get right even when they oversell the outcome: housing costs have outpaced wage growth by a wide margin, and for the right buyer, generating income from a property can make ownership viable when it otherwise wouldn't be. The strategy is real. The "living for free" part is just the clickbait version of it.

In 2026, the smarter question isn't whether house hacking works it's whether it's the right fit for you, your market, and your numbers.

Here's what that actually looks like.

What House Hacking Actually Means

House hacking is straightforward in concept: buy a primary residence and generate income from it to help offset the cost of owning it. The definition is that simple. The execution has a lot of range.The term got a lot of breathless social media attention a few years ago often paired with promises of "living for free" or "having your tenants pay your mortgage." That framing wasn't entirely wrong, but it oversimplified things in ways that set some buyers up for disappointment. In 2026, the more useful way to think about house hacking isn't about eliminating a housing payment. It's about engineering a more manageable one.

If a secondary suite generates $1,600 a month and the mortgage is $3,800, that $2,200 net payment might be very achievable where $3,800 wasn't. That's the real value not a free house, but a door that was otherwise closed, now open.

The Most Common Ways Buyers Are Doing It

The Secondary Suite Boom

Secondary suites basement apartments, laneway houses, garden suites, in-law suites have become the gold standard of modern house hacking in Canada, and the federal government has made significant moves to support them.The Canada Secondary Suite Loan Program, administered through CMHC, now offers homeowners up to $80,000 at a fixed rate of 2% over a 15-year term to build or convert a secondary suite double the program's original limit.¹ For buyers who need more borrowing power, CMHC's refinancing program allows homeowners to access up to 90% of their home's post-renovation value, which opens up more ambitious projects than a standard refinance would allow.²

Secondary suites have also become increasingly legal in places where they weren't before, as cities across Canada work to meet provincial housing targets. That regulatory tailwind, combined with federal financing support, makes this the most accessible entry point into house hacking for most buyers.

Multi-Generational Living

House hacking isn't always about renting to strangers. For a growing share of buyers, it means sharing a home and the costs that come with it with family.Multi-generational buying has been climbing steadily in Canada, driven by a convergence of forces: an aging population, affordability pressure that makes independent household formation increasingly difficult for young adults, and immigration patterns that prioritize family reunification. According to Statistics Canada's 2021 Census, the number of multi-generational households in Canada grew 21.2% over the preceding decade more than twice the overall rate of household formation.³ That structural shift has only accelerated since.

For families where the goal is housing an aging parent or a family member with a disability, there's an added financial incentive worth knowing: the federal Multigenerational Home Renovation Tax Credit provides up to $7,500 for constructing a self-contained secondary suite for a qualifying senior or adult. It's a meaningful offset on a renovation that was likely happening anyway.¹

The Classic Multi-Family

Buying a duplex, triplex, or small multi-family property and living in one unit while renting the others is the original form of house hacking and it still works in Canada. CMHC mortgage insurance allows buyers to purchase owner-occupied properties with as little as 5% down on homes up to $500,000, with the minimum down payment sliding to 10% on the portion between $500,000 and $999,999.² As of December 2024, the insured mortgage ceiling was raised from $1 million to $1.5 million, opening the door to more buyers in higher-priced markets.¹For those willing to share a property line with their tenants rather than just a backyard, the income potential is typically higher than a single secondary suite, and the strategy is time-tested.

The Honest Math

Here's the honest truth about house hacking in 2026: the "living for free" narrative that circulated on social media was never universally achievable, and it's even rarer now. Interest rates have come down from their peak but remain elevated compared to the pandemic-era floor. Home prices, while not climbing at the same frenetic pace as a few years ago, are not meaningfully lower in most major markets.That's not a reason to dismiss the strategy. It's a reason to recalibrate expectations.

The goal in 2026 isn't to eliminate a housing payment. It's to reduce it to something sustainable. In many cases, a well-chosen house hack turns an unaffordable property into a manageable one and that's a significant win. Buyers who run realistic numbers, factor in vacancy periods and maintenance costs, and approach the strategy with patience tend to do well. Buyers who chase optimistic projections tend to struggle.

Canadian lenders have also adapted. Rental income from owner-occupied multi-unit properties can be factored into qualifying income, subject to lender-specific guidelines and CMHC rules. The rules exist to keep the qualifying process grounded in real data they're a reasonable safeguard, not a barrier.

Who This Works Best For

First-time buyers facing an affordability gap. If income doesn't support the mortgage on a home that checks all the boxes, a property with rental potential can bridge that gap both by reducing the net monthly payment and, in qualifying scenarios, by improving what a lender will approve in the first place.The sandwich generation. Gen X buyers, often supporting aging parents while still raising or housing adult children have more motivation than any other group to maximise what a home does for them. A property designed for multi-generational living isn't just a financial strategy; it's a practical solution to a real caregiving reality. For families navigating the specific situation of housing a senior parent or a family member with a disability, the Multigenerational Home Renovation Tax Credit makes the financial case even stronger.¹

Future investors learning the ropes. Living in a property while managing a rental unit is one of the best ways to learn real estate investing without the full risk exposure of a standalone investment property. A buyer who spends two or three years in a house hack and then moves to their next home can keep the first property as a full-time rental with tenant management experience already under their belt.

What to Know Before Getting Started

Zoning and local regulations are non-negotiable. Secondary suite legality, short-term rental rules, and multi-family zoning vary dramatically by municipality. What's permitted three blocks away may not be permitted on the property being considered, and the rules are changing quickly as cities work to meet provincial housing targets. Unpermitted suites create liability headaches that outlast the savings they generate. Doing things by the book from the start isn't just the right approach it's the only one that holds up over time.Run conservative numbers. Plan for vacancies. Budget for maintenance. Use realistic rent estimates based on comparable properties in the neighbourhood, not best-case scenarios. If the math still makes sense when accounting for a month or two of vacancy each year plus routine repairs, it's a solid plan. If it only works at 100% occupancy with top-of-market rents, it's a risk.

Be honest about lifestyle fit. Sharing a property with tenants whether strangers renting a basement suite or family members in a multi-generational setup comes with real tradeoffs. It requires a certain temperament and a willingness to handle the occasional uncomfortable conversation. Buyers who go in with clear boundaries and realistic expectations tend to thrive. Those who underestimate the interpersonal dimension often don't.

The Bottom Line

House hacking is no longer a fringe idea for real estate investors. It's a mainstream strategy that serious buyers in 2026 are using to navigate a market that doesn't hand out easy answers. The fundamentals of homeownership building equity, gaining stability, and creating long-term wealth still hold. House hacking simply acknowledges that the path to those benefits sometimes requires a little more creativity with how a property is used.Every neighbourhood is different. Zoning rules, rental demand, and property potential vary widely, and the right house hack for one buyer might look completely different for another. If you're wondering whether you're the right fit for this strategy, that's exactly the conversation worth having. Reach out and let's dig into what it could actually look like for your market and your numbers.

Sources:

1. Government of Canada – Canada Secondary Suite Loan Program / Multigenerational Home Renovation Tax Credit:

2. CMHC Refinance for Building Secondary Suites / Homeowner Mortgage Loan Insurance:

3. Statistics Canada, 2021 Census of Population – Multigenerational Households:

2026 Home Design Trends: What's In, What's Out, and What Buyers Are Responding To [May 2026]

After a decade of cool grays, crisp whites, and spaces that looked more like showrooms than homes, buyers have changed what they're looking for. Call it quiet luxury the idea that richness comes from depth, craft, and intention rather than flash and excess. It's not maximalism. It's a shift toward spaces that feel like somewhere you'd actually want to live.

That shift is showing up in buyer data, listing descriptions, and design reports across the board. Here's what it looks like in practice and what it means if you're thinking about selling your home.

What's In

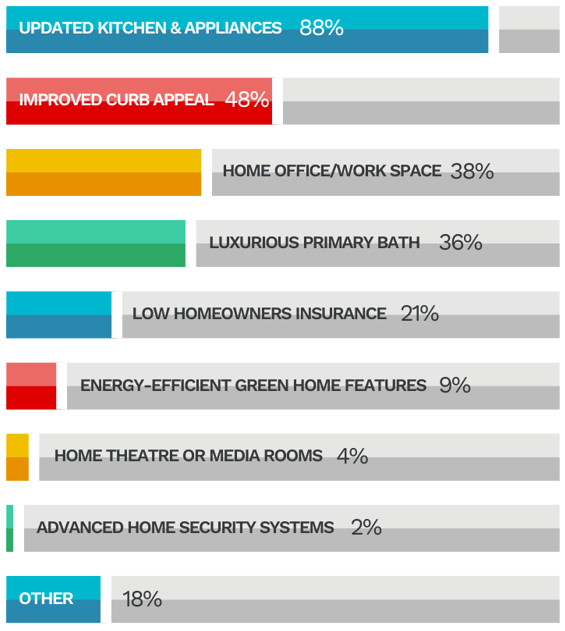

Color Is Back And It's Warmer Than You Think

The all-gray interior isn't just tired. Buyers have moved on. The biggest shift in Zillow listing descriptions over the last year has been a surge in "color drenching" coating walls, ceilings, and trim in a single immersive hue up 149% year over year.1 The direction is consistent across paint brands and design reports: warm beiges, caramels, terra cotta, sage green, and soft navy. A mix of '70s sunbaked tones and calming naturals.3

The psychology behind it makes sense. Buyers are increasingly seeking homes that feel like a sanctuary, not a showroom, and warm cohesive color is one of the fastest ways to create that. If you're thinking about selling your home, this has a practical implication: a single well-chosen paint refresh can dramatically change how a space photographs and how it feels at first walk-through.

The Art Deco Revival: Details That Stop the Scroll

Buyers are actively looking for character and that's showing up clearly in what design platforms are tracking. Houzz flagged the Art Deco revival as one of the defining trends of 2026, with searches for Art Deco interiors up 22% year over year.2 Think chevron patterns, brass accents, jewel tones, curves, arches, and scalloped edges that soften spaces and add visual depth. Listing mentions of "artisan craftsmanship" are up 21% and "vintage accents" up 17%.1The good news is this doesn't require a gut renovation. Arched doorways, a curved kitchen island, rounded furniture silhouettes, and detailed millwork can all deliver that effect. It's about adding one or two moments of character not redoing everything.

Surfaces and Materials That Make a Statement

Countertops and backsplashes are no longer meant to blend in. Natural stone, quartzite, marble, and travertine with soft sweeping veining is being used as a focal point rather than a background. Full-height backsplashes and dramatic stone applications create depth and warmth that photographs beautifully.2 Organic texture is showing up everywhere alongside it: plaster and limewash walls, sculpted surfaces, three-dimensional materials that shift with changing light.

Layered metals brushed brass paired with matte black and nickel signal a more evolved, curated take on the mixed-metals trend that's been building for a few years. The goal is intentional, not matched. Each finish feels chosen.

The Kitchen Is Getting Personal

Design professionals are nearly unanimous that the all-white kitchen has run its course.7,10 What's replacing it isn't one look it's the absence of a default. Warm neutrals, earth tones, and wood-grain cabinetry are taking over from painted finishes, and the transitional style has settled in as the most popular direction, with the farmhouse kitchen continuing to lose ground it's unlikely to recover.5

The bigger shift underneath all of it is personalization. Buyers want to see a kitchen that feels considered not one that played it safe. A walk-in pantry, an unexpected cabinet color, a stone backsplash that runs floor to ceiling: these are the details that make a kitchen feel like it belongs to someone, which turns out to be exactly what buyers are looking for.

Open Concept Grew Up

Open floor plans aren't going away but buyers no longer want an undifferentiated box. Buyer preferences have shifted toward layouts that offer both flow and definition spaces that feel connected but serve a clear purpose.4 What's rising is the semi-closed floor plan: subtle architectural separation between the kitchen, dining room, and living areas that maintains connection while creating intimacy. The flexibility of how a home's space is organized now matters more to buyers than the raw square footage it contains.12Remote work is a big part of why. When your home is also your office, privacy has real value. Dedicated home offices are consistently one of the most requested features this year, and mentions of "reading nooks" quiet, defined personal spaces are up 48% in Zillow listing descriptions.1 If you're thinking about selling and you have a defined dining room, a separate office, or distinct living zones, don't apologize for them. Stage and describe each space as intentional. Buyers are looking for purpose, not just square footage.

Homes That Are Designed to Feel Good

One of the quieter shifts in how buyers evaluate homes is the move toward what designers call wellness design the idea that a home's layout and materials should actively support how you feel in it, not just how it looks. It's less about a single feature and more about an overall sensibility: does this space help you rest, focus, and decompress, or does it just look good in photos?That sensibility is showing up in listing language in measurable ways wellness mentions are up 33% year over year, and spa-inspired bathrooms have climbed 22%.1,8 But the concept has expanded well past the primary bath. Biophilic design bringing in natural light, organic materials, living plants, and visual connections to the outdoors has become a core consideration because it addresses the same underlying need: buyers want to feel better in their homes.9 So does circadian lighting that shifts with the time of day, and dedicated spaces designed specifically for quiet a reading corner, a window seat, a nook that actually gets used.

These aren't luxury add-ons anymore. They're showing up in mainstream listings because people are prioritizing how their home makes them feel on a Tuesday afternoon, not just how it presents at a party.

Resilient and Efficient Homes: The Practical Side of 2026 Design

Climate reality is showing up in listing data in a way that's hard to ignore. Features like flood protection, fire-resistant landscaping, and whole-home battery systems are all climbing fast and 86% of buyers now say it's very important that a home be "climate-proof."1 Zero-energy-ready homes have surged 70% in Zillow listing mentions, with whole-home batteries up 40% and EV charging up 25%.1Energy efficiency is part of the same conversation. Buyers are evaluating solar readiness, EV chargers, and efficient HVAC systems the same way they evaluate a kitchen renovation — as a financial consideration, not just an environmental one. Utility costs, insurability, and long-term resilience are all factored in. If you're thinking about selling and you have any of these features, make sure they're documented clearly in your listing. Buyers are actively reading for this language, and homes that speak to it stand out.

What's Out

Design trends don't just tell you what to add they tell you what to address before you list. A few things buyers have clearly moved past:- All-gray everything. Functional for a decade, now forgettable. Buyer sentiment has shifted clearly away from both cool gray and stark white as default palettes. Sterile, clinical spaces read as dated now, not clean.2,3

- The overdone farmhouse look. The aesthetic isn't dead, but the version heavy on purely decorative elements shiplap for the sake of shiplap, barn doors on every opening has peaked. What's replacing it is a warmer, more grounded approach leaning on authentic materials over surface-level styling.

- Themed bonus rooms. "Man cave," dedicated wine rooms, home theaters with no other use buyers want rooms that flex, not rooms that commit to a single identity. Spaces that can't be repurposed read as liabilities now, not amenities.

- Two-story foyers. They create a striking visual, but the trade-offs have caught up with them. NAHB data shows 32% of buyers are likely to reject a home with a two-story foyer outright, while only 13% consider it a must-have.6 The energy inefficiency, heat imbalance, and lost usable square footage are no longer worth the entrance moment.

- Matched-finish everything. Coordinating every fixture, cabinet pull, and faucet to a single metal finish now reads as a 2015 renovation. The shift is toward intentionally layered metals brushed brass, matte black, and nickel that feel collected over time rather than sourced from the same catalog page.

- Open shelving as a kitchen default. What looked fresh a few years ago now reads as high-maintenance and visually noisy to a lot of buyers. The enthusiasm for it has cooled significantly, and the backlash is real enough that agents are recommending sellers address it before listing.11

- Safe "greige" tile that disappears into the background. Surfaces are meant to make a statement now, not blend in. Full-height backsplashes, dramatic stone, and layered finishes have replaced the disappearing neutral as the standard expectation in well-presented kitchens and baths.

- Maximalism for resale. Rich, layered, highly personal spaces can be genuinely beautiful to live in but they're difficult to sell. Buyers need to be able to see themselves in a space. Heavy personalization, bold collections, and visually dense rooms make that harder, which tends to show up in longer days on market and more negotiated offers.

What Changes and What You Leave Alone

Not every item on this list requires a contractor. A $500 to $2,000 refresh can meaningfully shift how a home is perceived: paint in a warm current tone, swapping out dated light fixtures, updating hardware from chrome to brushed brass or matte black, adding a limewash accent wall in a key space. These are cosmetic moves but they change how a home feels, and that feeling is what drives buyer interest from the very first look.That first look is doing more work than most sellers realize. Warm, textured, layered spaces photograph better than stark white minimalist ones and since most buyers have already formed a strong impression before they ever step inside, the visual presentation of your home directly affects how fast it moves and what kind of offers it generates.

Buyers are deciding in seconds. The goal is to design for the feeling they get at first scroll not the trend you were following three years ago.

If you're thinking about preparing your home to sell and want to know which updates are worth making in your specific price range and neighborhood, reach out. That's exactly the kind of conversation that can make a real difference in your results.

Sources

1. Zillow – Spotted on Zillow: Six Home Trends To Follow in 20262. Houzz – Sneak Peek: Houzz Reveals 11 of the Top Home Design Predictions for 2026

3. Axios – 2026 home design trends: Zillow and others reveal picks

4. RoylinSells – Are Open Floor Plans Still Popular in Today's Housing Market?

5. Houzz – 2025 U.S. Houzz Kitchen Trends Study

6. NAHB – Two-Story Foyer Trend Stabilizes in 2024

7. Fixr – Kitchen Design Trends Report 2026

8. Fixr – Bathroom Design Trends Report 2026

9. Tami Faulkner Design – Top Custom Home Design Trend 2026

10. NKBA – 2026 Design Trends Report

11. GoBankingRates – 6 Key Design Trends That Are Make-or-Break for Homebuyers in 2026

12. BHGRE – 2026 Design Trends Moving Real Estate

Is Buying a Home Together Right for Your Family? How to Approach Multigenerational Living [April 2026]

For a long time, multigenerational living had a reputation problem. It was the option families turned to when something had gone wrong a job loss, a divorce, a health crisis. Moving back in with your parents, or having your parents move in with you, meant something hadn't worked out.

That story has changed pretty significantly.

Today, families are choosing this arrangement on purpose, not as a fallback, but as a deliberate decision to share costs, stay connected, and build something that actually works for how their lives are structured right now. The latest Statistics Canada data shows that nearly 1 in 5 Canadians lives in an intergenerational household made up of parents and adult children and that number has been growing. [1] These aren't people making the best of a bad situation. They're rethinking what "home" needs to do.

If this is something you're considering or something a family member has brought up here's what's worth knowing before you start the search.

Why More Families Are Going This Route

The honest answer is: it's rarely just one thing.For most families, cost is somewhere in the mix. With the GTA average home price sitting above $1.0M and nearly half of Canadians reporting serious concerns about housing affordability, buying together has become a practical response to a market that makes solo homeownership increasingly hard to pull off. [2][3] More people on the mortgage means more income to qualify with, and more people splitting costs means the monthly number gets a lot more manageable.

There's also a wrinkle specific to how mortgages work in Canada that doesn't get talked about enough in this context. Mortgage terms typically renew every four or five years, and the Bank of Canada has flagged that roughly 60% of outstanding mortgages will renew in 2025 or 2026 with many borrowers facing meaningfully higher payments than they had before. [4] For some families, buying together isn't just about getting in. It's about staying in comfortably when renewal comes around.

Caregiving is the other big driver that doesn't always make it into the conversation upfront. Canada now has over 8 million people aged 65 and older, and the question of how families want to handle aging parents isn't one most people want to outsource entirely. [5] For the families who've actually made multigenerational living work, being close enough to help and being helped is often what they're most grateful for in hindsight.

Remote work has also quietly shifted the geography of family life. When you're not tethered to an office five days a week, being near family becomes less of a professional sacrifice. About 1 in 4 employed Canadians is now in either a fully remote or hybrid arrangement, which means more families can actually act on the instinct to live closer together. [6]

And then there's the harder-to-quantify stuff the daily support, the shared routines, the sense that you're not navigating things alone. If you find yourself drawn to this idea, your reasons are probably more layered than just the numbers.

What to Actually Look for in a Property

This is where a lot of families get tripped up. They find a house they love, start imagining how it could work, and convince themselves the layout is more flexible than it really is. Then six months into living together, they realize what they actually needed was a separate entrance not just a second bathroom.The properties that work best for multigenerational living tend to share a few things in common.

They take privacy seriously. Not just in theory, but in the layout. Dual primary suites, separate entrances, a finished basement with its own living area, or a self-contained secondary suite these aren't luxury features, they're what make the arrangement actually sustainable. If each household can't fully decompress, host their own guests, and keep their own rhythm, the togetherness part gets old fast.

They're built or can be converted for flexibility. Secondary suites, laneway homes, and garden suites have become a much bigger part of this conversation as municipalities across Canada loosen their rules around additional units. If a self-contained space isn't already in place, it's worth asking whether the lot and local zoning would make one possible down the road. That kind of optionality has real value.

They work for the long game. Think about where everyone in the arrangement will be in ten or fifteen years. First-floor suites, wider hallways, zero-step entries, and rooms that can adapt as needs change aren't just nice to have, they're what make a multigenerational home function well over time rather than just right now. StatsCan data shows that home adaptations are already a reality for a significant share of older Canadians, and that need only grows. [7]

The short version: the best multigenerational properties support both togetherness and independence. If a home checks one but not the other, keep looking.

The Conversations Most Families Skip

Here's the part that tends to get glossed over, because the emotional pull of the idea is strong and the practical details feel like they can wait. They can't.Start with the financial structure early. If multiple people will be on the mortgage, everyone needs to understand what that actually means. Combining incomes can help qualify for more, but it also means everyone on the mortgage shares legal responsibility for the debt and everyone is exposed to renewal risk together. That's a meaningful commitment worth sorting out before you fall in love with a property. [4]

Define ownership clearly. Title can be held as joint tenancy or tenancy in common, and those aren't just legal technicalities they affect what happens if someone wants to sell, if a relationship changes, or if one owner passes away. Equal contributions don't automatically mean equal ownership makes sense, and unequal contributions don't mean anyone is getting a bad deal. But these things need to be spelled out explicitly, not assumed.

Don't overlook closing costs. Land transfer tax varies by province and, in some cities, stacks with a municipal layer on top. If first-time buyers are part of the purchase, it's also worth a conversation about tools like the First Home Savings Account, the Home Buyers' Plan, and the Home Buyers' Amount — real savings that are easy to leave on the table if nobody brings them up. [8][9][10]

Get it in writing. A verbal agreement between family members feels fine when everyone is on the same page. It gets complicated when circumstances change and circumstances always change eventually. A written agreement covering shared expenses, maintenance responsibilities, use of common areas, and how an exit would be handled gives everyone protection, and honestly, usually makes the conversations easier because you've already had them.

Talk through the "what-ifs" before closing. Job changes, caregiving shifts, a marriage, someone wanting to sell, or payments rising at the next mortgage renewal, these aren't worst-case scenarios, they're just life. Who carries the renewal risk, and what happens to the arrangement if carrying costs go up? Getting those answers sorted before you sign is much easier than trying to work it out once you're already living together.

One more thing worth knowing: if the arrangement involves creating a self-contained unit for an eligible family member, the Multigenerational Home Renovation Tax Credit can cover qualifying renovations up to $50,000, with a refundable credit of up to $7,250 per claim. [11] It's not the reason to do this but it's worth knowing it exists.

This stuff isn't fun to work through. But families who do it upfront tend to have far smoother experiences than those who assume it'll all work itself out.

Is This Actually the Right Move?

That depends on a few honest questions.Is everyone genuinely choosing this, or is someone going along with it? The families who thrive in multigenerational arrangements almost always went in with shared intent everyone wanted it, everyone understood what they were agreeing to. That's different from one party tolerating it because the math made sense or because it felt like the easier thing to say yes to.

Are the financial expectations clear and actually fair? Not just the down payment, but ongoing contributions, equity stakes, closing costs, and what happens if someone needs to exit. These things are much easier to define before the purchase than to renegotiate afterward.

Does everyone have a realistic picture of what shared space feels like day-to-day, long-term? Not on a good weekend when everyone's happy to be together but on a random Tuesday when someone's had a bad day, the kids are loud, and you just want your home to yourself for an hour.

If the answers to those questions are honest and mostly positive, multigenerational living can be genuinely great. Plenty of Canadian families have made it work extremely well.

BOTTOMLINE

Multigenerational living has moved from fallback plan to deliberate strategy for a growing number of Canadian families and it's easy to understand why. The affordability pressure is real, the caregiving benefits are real, and with mortgage renewal cycles adding a layer of financial uncertainty that's worth planning around, sharing a home has become a genuinely smart option for a lot of households.What makes it work is going in with eyes open: the right property, the right legal structure, and honest conversations before anyone signs anything.

If this is something your family is exploring or if it's on the horizon and you're not sure where to start that's exactly the kind of conversation a good local agent, lender, and lawyer or notary can help you think through together. Getting the strategy right early makes everything that follows a lot smoother.

Reach out anytime even if you're just starting to think it through.

Sources

[1] Statistics Canada, Adulting together: Parents and adult children who co-reside

[2] Statistics Canada, The Daily Social geography: A special edition of Insights on Canadian Society

[3] Canadian Real Estate Association (CREA), National Statistics February 2026

[4] Bank of Canada, Financial Stability Report 2025

[5] Statistics Canada, Older adults and population aging statistics

[6] Statistics Canada, The Daily Labour Force Survey, November 2024

[7] Statistics Canada, Aging in the community: Factors associated with home adaptations

[8] Canada Revenue Agency, First Home Savings Account (FHSA)

[9] Canada Revenue Agency, The Home Buyers' Plan (HBP)

[10] Canada Revenue Agency, Line 31270 Home buyers' amount

[11] Canada Revenue Agency, Multigenerational Home Renovation Tax Credit (MHRTC)

What Actually Makes a Listing Stand Out in 2026 [March 2026]

The playbook for selling a home has changed fast. Buyers have more options, more leverage, and they are using it.

According to the Canadian Real Estate Association (CREA), active listings on Canadian MLS® Systems were up 7.4% year-over-year at the end of 2025.¹ At the same time, the national MLS® Home Price Index declined 4% year-over-year by December 2025, with benchmark prices falling for seven consecutive months.²

What does that mean for sellers? It means the days of snapping a few photos, putting the home online, and waiting for offers are over. Today's buyers are more informed, more cautious, and more willing to walk away. The listings that win are the ones that eliminate friction at every stage from the first scroll to the final offer.

Here is what that actually looks like.

Know What the 2026 Buyer Is Filtering For

Before we talk strategy, it helps to understand what is driving buyer decisions right now. It is not just about bedrooms and bathrooms anymore. Today’s buyer is thinking about what a home will cost them after they buy it.Layout and Function Over Size

According to Better Homes & Gardens Real Estate’s 2026 Design Trends Report, 86% of buyers say flexible layouts help them see past square footage. Dedicated home offices, walk-in pantries, multipurpose rooms, these features outweigh raw size. Nearly half of buyers in that same study said they will not buy a home that does not feel right the moment they walk in.³Move-In Ready Is Increasingly Non-Negotiable

Home inspections remain one of the leading reasons conditional sales fall apart. In a market where buyers have more choices and tighter budgets, surprise repair costs are a deal-breaker. Financially stretched buyers are not looking to absorb risk, they are looking for reasons to walk away.The tolerance for deferred maintenance has evaporated. Buyers are already stressed about affordability. When a buyer sees deferred maintenance, they do not see “potential.” They see risk. Agents across the country report that buyers are increasingly requesting price reductions or closing cost credits based on inspection findings and in a balanced-to-buyer’s market, they have the leverage to get them.

Energy Efficiency as a Financial Filter

Energy efficiency is being evaluated as a financial hedge against utility costs, against climate risk, against future insurability. Canada’s EnerGuide rating system, backed by the Government of Canada through Natural Resources Canada, gives buyers a standardised way to compare the energy performance of homes.⁴ An EnerGuide label is increasingly becoming part of the buying conversation, and programmes like the Canada Greener Homes Initiative have raised awareness of what energy efficiency actually means in dollars saved.Sellers who understand this can position features like updated HVAC systems, new windows, or solar panels not as nice-to-haves, but as cost-saving assets.

The bottom line: sellers who understand this mindset can position their listing to meet it head-on.

Win the Screen Before You Win the Showing

The online listing is the first showing. By the time a buyer walks through the front door, they have already decided they are interested or they have scrolled past.The First Photo Is Everything

85% of homebuyers consider listing photos the most critical factor when evaluating a property online.⁵ Not the price. Not the description. The photo.Listings with professional photography receive up to 61% more views and sell 32% faster.⁵ In a market where inventory is rising and buyers are choosier, professional photography is an enormous opportunity for sellers who take presentation seriously.

Go Beyond Standard Photography

Going above and beyond can garner even more attention for your home. Twilight photos used as the primary listing image average 76% more views.⁵ Homes with aerial or drone photos can often sell faster.⁶ Listings with video get 403% more inquiries.⁶These are not small edges. In a market where buyers have more options, these are the differences that help a listing generate momentum.

3D Tours Are Becoming Expected

Virtual tours do two things at once. They filter out unqualified buyers before they waste anyone’s time. And they give serious buyers the confidence to move faster when they do show up in person. In fact, listings with 3D virtual tours sell up to 31% faster and for up to 9% more.⁷·⁸The visual package for a listing is doing the work of an open house before anyone sets foot in the property. If the first photo does not stop the scroll, the square footage and the price will never get a chance to matter.

Remove Every Reason to Say “No”

In a slower market, uncertainty creates lower offers or no offers. Every unanswered question is a reason to negotiate down or walk away.The smartest move? Answer the scary questions before they are asked.

That starts with a pre-listing inspection. For $300 to $700, a seller can identify and address issues on their own timeline and terms before a buyer’s inspector turns a minor finding into a deal-killing negotiation.⁹ More agents and brokerages across Canada are actively encouraging this approach, recognising that a pre-listing inspection gives sellers the opportunity to address repairs, set a fair price, and build buyer confidence before the listing even goes live.¹⁰Beyond the inspection, consider providing the ages of major systems (HVAC, roof, water heater), a 12-month utility cost history, and documentation of any recent repairs. This is not about over-sharing. It is about removing the discount that buyers are mentally applying for risk and uncertainty.

Photos win hearts. Data wins brains. A winning listing needs both.

Price It Right or Pay the Price

Everything above understanding the buyer, presenting beautifully, being transparent leads here. Pricing. Overpriced listings do not just sit longer. They sell for less than if they had been priced correctly from the start.The Overpricing Trap

In 2025, the national MLS® Home Price Index fell 4% year-over-year, with Ontario and British Columbia seeing benchmark declines of 5.6% and 6.4% respectively.² Sellers who made price concessions to close before year-end pulled those numbers further down.¹When a listing sits, days on market climb and buyers start to assume something is wrong even when the only issue was the price. That stigma is real and hard to undo. Buyers begin to wonder what they are missing.

The First Two Weeks Are Everything

A listing’s visibility and buyer interest peak immediately after launch. Pricing high to see what happens is dangerous every week of inactivity makes the next correction less effective.Pricing competitively from the start can attract multiple offers and often results in a higher final sale price. The goal is not to leave money on the table by underpricing. The goal is to price with precision, right at the point where serious buyers recognise value and act fast.

One Bold Move Beats Death by a Thousand Cuts

Multiple small reductions signal desperation and train buyers to wait for the next drop. A single strategic correction, aggressive enough to restart the clock, is almost always more effective.Homes with repeated small reductions typically sell for significantly less as a percentage of original list than those with one well-timed adjustment. The market reads hesitation as weakness.

Pricing correctly from day one is not conservative. It is strategic. And it is one of the most valuable things a good agent brings to the table.

The New Definition of a Winning Listing

The 2026 winner is not the cheapest or the biggest. It is the most ready.Prepared with the buyer’s mindset in mind. Presented with scroll-stopping professional media. Supported by transparency that builds confidence. Priced with precision from day one.

That is the new bar. Meet it, and your listing competes. Miss it, and you are watching it sit.

If you are thinking about selling or if you have a listing that is not performing the way you expected, let’s talk. The difference between a home that moves and one that sits often comes down to strategy, not the property itself.

Sources

1. CREA – Home Sales in Canada End 2025 Quietly

2. WOWA – Canadian Housing Market Report, January 2026

3. Better Homes & Gardens Real Estate – 2026 Design Trends Report (via HousingWire)

4. Natural Resources Canada – EnerGuide Energy Efficiency Home Evaluations

5. PhotoUp – Hot Real Estate Photography Statistics You Need to Know in 2025

6. RubyHome – Real Estate Photography Statistics”

7. Matterport – “With 3D Tours, Properties Sell Up to 31% Faster and at a Higher Price

8. Matterport – New Study Shows Property Buyers and Sellers Overwhelmingly Prefer Listings with 3D Tours

9. nesto.ca – Home Inspection Fees & Services in Canada

10. AmeriSpec of Canada – Pre-Listing Inspection

The True Cost of Homeownership: What You Pay Beyond the Mortgage [Feb 2026]

When many new homebuyers calculate whether they can afford a new home, they focus almost exclusively on one number: the monthly mortgage payment. It's the figure lenders use for the mortgage stress test, the number real estate agents discuss during showings, and the benchmark buyers use to determine their budget.

However, the mortgage is only the starting line. Homeowners also pay for property taxes, insurance, utilities, maintenance fees, surprise repairs and ongoing maintenance. According to housing cost breakdowns from Ratehub, these non-mortgage expenses can easily add $1,500 or more per month on top of the mortgage, depending on the home and location. When you factor in these costs, a $3,000 monthly mortgage can quickly push total housing expenses well beyond $4,500 per month.¹

So while qualifying for a mortgage answers one question, "Can a bank trust you with this loan?", it doesn't answer the more important one: "Can you comfortably maintain this lifestyle?"

In today’s market, about one in four Canadian homebuyers report experiencing at least some post-purchase regret.² While most homeowners remain satisfied, research shows that regret often emerges when the true cost of ownership, such as maintenance, repairs, and ongoing living expenses was higher than expected. To reduce the risk of buyer’s remorse, it’s critical for homebuyers to plan not just for the mortgage payment, but for the full cost of living in the home.

The Predictable Ongoing Costs

Property Taxes

Property tax bills have been rising in many cities as municipalities work to fund infrastructure and services. In 2024, the median year-over-year change in property tax rates among 24 major Canadian cities was about 4.9 percent, with some regions experiencing even greater increases.³Property taxes aren’t fixed. Reassessments and rate changes happen regularly, and as neighbourhood values rise, so do tax bills even when the rate stays the same.

Home Insurance

As of 2026, home insurance premiums have entered a “new normal.” Record weather-related losses in 2024, combined with higher rebuilding and replacement costs, continue to push insurers to raise rates and reassess risk across many regions.⁴In provinces like Alberta, home insurance premiums have increased by nearly 90% over the past decade, with similar upward pressure emerging nationwide.⁵ As insurers recalibrate risk at the postal code level, homeowners can see their premiums rise $100–$200 per month in a single year, even without making a claim or changing coverage.

Condo Maintenance Fees

For buyers entering the condo market, monthly fees typically range from $0.60 to $1.00 per square foot, depending on the building and amenities.⁶ These fees are mandatory and are used to fund day-to-day operations as well as long-term reserve funds for major repairs.Unlike the US where HOA fees are often optional community amenities, Canadian condo fees are mandatory contributions that prevent catastrophic special assessments later.

Utilities

Homeowners should budget between $250 to $600 monthly for utilities including electricity, heating, water, internet, and phone services, with costs varying based on your home's size and location.1These expenses often come as a surprise to first-time buyers, particularly those transitioning from apartment living where some utilities may have been included in rent. Larger homes naturally require more energy for heating and cooling, while properties with outdoor spaces may see higher water usage during warmer months.

The "Commuter Tax"

There's also what might be called "the commuter tax." Moving to suburban markets for a cheaper house can increase gas and transit costs that often negate the mortgage savings. That $300,000 price difference disappears quickly if you're spending an extra $400 monthly on various Transits, gas and/or Highway 407.Routine Maintenance

Beyond emergencies, Canadian homes require ongoing care: lawn service, gutter cleaning, pest control, HVAC servicing, snow removal, and seasonal tasks. These aren't luxuries for many households they're practical solutions to time constraints and property upkeep in Canada's demanding climate. Collectively, these services can add $200-400 monthly to ownership costs.The Irregular, but Inevitable Expenses

Major System Replacements

This is where many Canadian homeowners get caught off guard. Maintenance and repairs aren’t a matter of if but when and rising labour and material costs have made these repairs significantly more expensive in recent years.According to Statistics Canada and industry cost reports, home repair and maintenance costs have increased materially since 2018, driven by construction inflation and labour shortages.7 As a result, homeowners are commonly advised to budget 1% to 2% of their home’s value annually for maintenance and long-term repairs.8

Major system replacements can add up quickly:

- Roof replacement: $8,000–$15,000+9

- HVAC (furnace or heat pump): $5,000–$12,00010

- Water heater: $1,200–$2,50011

- Foundation repairs: $4,000–$15,000+12

Use the inspection as a planning tool. A 15-year old furnace or aging roof signals $8,000-15,000 in likely expenses within the first few years. That's not a deal-breaker, it's a budget roadmap. Buyers who understand these timelines can plan strategically instead of scrambling when systems fail.

Canada's climate makes this worse. The "freeze-thaw" cycle can hurt some roofs, driveways, and foundations faster than most international climates. A roof that might last 25 years in Arizona may need replacement after 15-18 years in some provinces.

Newer isn't maintenance-free. Newer builds offer a temporary reprieve, but systems still age, warranties expire, and eventually every home requires major capital improvements.

Emergency repairs happen at the worst times. An HVAC failure during a cold snap, a burst pipe in winter, or ice dam damage to the roof, these scenarios happen when it's least convenient and most expensive. Without liquid reserves, a single emergency can derail finances entirely.

Ownership Costs That Creep Up Over Time

Here's what surprises many first-time buyers: the so-called "fixed costs" of homeownership aren't actually fixed.While a locked-rate mortgage provides payment stability for your term (typically 5 years), the other components, taxes, insurance, and condo fees can climb significantly year over year due to inflation, climate risk, and local policy changes. A mortgage payment that felt comfortable at closing can feel tight three years later, even without lifestyle changes.

The "2026 Renewal Wall" presents a significant challenge for homeowners. Large % of outstanding mortgages were and are expected to renew in 2025 or 2026, with many owners facing substantial payment increases.13 Unexpected costs go beyond just maintenance and repairs. Many homeowners will experience sticker shock when their mortgage payments reset at higher rates upon renewal.

The same gradual creep affects utilities, maintenance services, and every other aspect of homeownership.

Planning Smarter: How Canadian Homeowners Can Stay Ahead

The encouraging news: buyer's remorse is largely preventable. The issue isn't buying the wrong house, it's buying without adequate financial preparation for what homeownership entails.Create a Dedicated House Repair Fund

Separate from emergency savings, this fund exists solely for home maintenance and repairs. Treat it like a non-negotiable monthly bill, set up automatic transfers so it happens without thinking about it.The old rule of saving 1% of your home's value annually for repairs? It's proving insufficient for some homeowners, particularly those with older properties or homes experiencing extreme weather. Aim for 2% if possible. For a newer home with recent updates, less might suffice. For an older property or one with systems nearing end-of-life, you’ll likely need to plan for greater costs.

Don't Drain Your Savings at Closing

Cash reserves protect against surprises and prevent forced debt when repairs arise. If possible, keep a liquid emergency repair fund after closing rather than putting every available dollar into the down payment or immediate renovations. That breathing room matters more than most buyers realize.Invest in Preventative Maintenance

Annual furnace servicing, gutter cleaning, and seasonal inspections catch small problems before they become expensive emergencies. A modest service call that prevents a major system failure is always worthwhile.Create a seasonal maintenance calendar: HVAC checkups in spring and fall, gutter cleaning before winter, roof inspections after major storms. Consistency prevents costly surprises.

Leverage Canadian Tax Advantages

Consider leveraging Canadian tax advantages to build these reserves. First-time buyers should keep their FHSA (First Home Savings Account) open after purchase, or use the tax refund generated by it to seed their repair fund. The tax benefits you received while saving for the down payment can continue working for you as a homeowner.Know Your Home's Systems and Timelines

Understanding when major systems were last replaced helps predict future expenses. A 15-year-old water heater isn't an emergency today, but it signals a likely expense within the first few years of ownership. Planning beats scrambling.Why Homeownership Still Makes Sense

Despite the expenses, homeownership remains one of the most powerful wealth-building tools available to families when approached correctly.Long-Term Equity Building

Mortgage payments build equity with every payment. Unlike rent, ownership creates a forced savings mechanism that compounds over decades. In most markets, homes appreciate over time, multiplying the wealth-building effect.

Stability and Control

Homeowners control their living environment. Want to renovate the kitchen, paint the walls, landscape the yard, or install solar panels? Ownership provides autonomy that renting never will. That control has both lifestyle and financial value.Predictability vs. Rent Volatility

While ownership costs rise gradually over time, rent increases can be sudden and dramatic. A fixed-rate mortgage provides a level of predictability that the rental market cannot match.Yes, taxes and insurance increase, but the principal and interest portion typically 60-70% of the total payment remains locked for your term. Renters face volatility on 100% of their housing costs.

Lifestyle Benefits

Beyond finances, homeownership offers intangible benefits: deeper community roots, stability for families, space for hobbies, and the pride of building something that's truly yours. These benefits have real value, even if they don't appear on a balance sheet.The key is ensuring the financial foundation supports the lifestyle, not undermines it.

A Better Way to Think About Affordability

The true measure of affordability isn't what a lender will approve, it's what allows you to sleep well at night when the furnace fails or your mortgage comes up for renewal.The smartest buyers calculate affordability as "mortgage plus carrying costs" from the start. This might narrow the price range slightly, but it creates breathing room and peace of mind that makes a house feel like a home.

Homeownership remains one of the most powerful wealth-building tools available to families, but only when approached with financial realism rather than maximum leverage. Having an honest conversation about what affordability truly looks like isn't about limiting dreams, it's about making sure those dreams don't become financial nightmares.

Sources:

1. Ratehub, Additional Monthly Costs of Homeownership

2. Wahi 2024 Homeowner Happiness Survey

3. Zoocasa, Canada’s Property Taxes 2024 National Snapshot

4. Harvard Western Insurance, Weather Damage Drives House Insurance Rates Up in Canada

5. Pembina Institute, How Governments and Insurers Can Help Lower Soaring Home Insurance Costs

6. Precondo, Maintenance Fees for Condos in Canada

7. Statistics Canada, Which households need repairs, and how much more do they cost?

8. Ratehub, How Much Should You Budget for Home Maintenance?

9. Homestars — Roof Replacement Costs in Canada

10. Custom Contracting, How Much Does HVAC Installation Cost in Ontario?

11. HomeAdvisor (Canada, Water Heater Installation Cost

12. Homestars, Foundation Repair Costs

13. Bank of Canada, How Will Mortgage Payments

2026 Canada Housing Market Forecast: Will Buyers Finally Re-Enter the Market? [Jan 2026]

Will 2026 be the year Canadian buyers stop waiting? Most major housing forecasters believe activity will finally pick up after two muted years, but expectations vary on how strong that rebound will be and where it will show up first. After a sluggish and uncertain 2025, the Canadian housing market appears positioned for gradual normalization rather than a sharp recovery.

The Canadian Real Estate Association (CREA) now forecasts national home sales of roughly 509,000 transactions in 2026, representing about 7–8% growth year over year. 1,2 That would place activity above 2025 levels, though still below long-term historical averages. Average prices are expected to return close to the $700,000 range, reflecting modest appreciation rather than a renewed surge. 1,3

The 2025 Context: A Delayed Recovery, Not a Breakdown

In early 2024, CREA projected that 2025 would mark a meaningful rebound year for Canada’s resale market, driven by pent-up demand and easing interest rates.1 By late 2024, that recovery appeared to be forming. Under that forecast, national home sales were expected to exceed 500,000 transactions, with national average prices climbing back toward $700,000.That momentum stalled in early 2025. Trade uncertainty, broader economic unease, and affordability pressures pushed many buyers back to the sidelines, prompting CREA to downgrade its outlook.4 Sales activity softened most noticeably in British Columbia and Ontario, while prices in several major urban markets came under renewed pressure.4,10

Importantly, the market did not deteriorate further. Beginning in spring 2025, CREA data showed a showed continued improvement in sales activity, suggesting that demand was delayed rather than destroyed.⁵ The result is a downward revision to 2025 forecasts, but solid upward momentum heading into 2026, with last year’s 2025 expectations now effectively pushed out one year.1,4

2026 Forecasts: Where Canadian Forecasters Agree and Disagree

Sales Activity: Gradual Thaw, Not a Flood

Sales forecasts for 2026 cluster more tightly in Canada than in the U.S., but uncertainty remains. CREA’s national forecast implies high-single-digit growth, bringing sales back into the low-500,000 range.1,2 RE/MAX Canada similarly expects increased activity, citing improving consumer confidence and buyers adjusting to current financing realities.9The central uncertainty is not economic capacity but psychology. Many Canadian buyers spent the past two years waiting for more aggressive rate cuts or price declines. As those expectations fade, the decision to re-enter the market increasingly hinges on life events, job changes, family needs, downsizing, or relocation, rather than market timing.3,7

Unlike the pandemic rebound, 2026 is unlikely to bring a surge of speculative or urgency-driven buying. Instead, forecasters expect incremental increases in transaction volume, market by market, price tier by price tier.9,14

Home Prices: A Tug-of-War Between Growth and Correction

Price forecasts for 2026 reveal a rare divergence among Canada’s top housing analysts, signaling a market in transition. While the consensus points to stability, experts disagree on whether the national average will tick up or drift slightly lower.CREA projects the national average home price to rise roughly 3.2% in 2026, returning close to the $700,000 mark.1,2 This aligns with Royal LePage’s outlook, which forecasts aggregate price growth of approximately 1%, supported by steady demand in more affordable provinces.7

However, not all outlooks are positive. RE/MAX Canada stands as a notable outlier, forecasting a national average price decline of roughly 3.7%, despite rising sales activity.9 This bearish view highlights the heavy weight of inventory buildup in Canada’s most expensive markets.

The "Two-Speed" Market Continues Regardless of the national average, all forecasters agree on a widening regional gap:

- The Correction Markets: Higher-priced regions like Greater Toronto and Greater Vancouver are expected to see flat to negative price movement. Here, affordability ceilings have been hit, and listing inventory is rising faster than sales.7,8

- The Growth Markets: In contrast, affordable regions, specifically Alberta, Quebec, and Atlantic Canada are forecast to outperform. These markets continue to attract inter-provincial migration and offer entry points that first-time buyers can actually afford.7,8

Interest Rates and Affordability: Stability Over Relief

Unlike the U.S., Canadian mortgage expectations hinge on Bank of Canada policy rather than long-term bond-market forecasts. Current consensus suggests the policy rate is nearing a plateau, with rate cuts largely behind us and borrowing costs expected to remain relatively stable into 2026.12,13For buyers and sellers, this means rate stability matters more than rate relief. While borrowing costs may ease modestly, affordability improvements are expected to come gradually through income growth and slower price appreciation rather than dramatic financing changes.3,13

The practical implication mirrors the U.S. experience: waiting for a return to 2020–2021 conditions is increasingly unrealistic. The market is adjusting to a higher-rate baseline, and participants must plan accordingly.3,7

What This Means for Buyers

For buyers, 2026 offers improved conditions compared with the past two years—but not a buyer’s market across the board. Inventory has increased modestly, competition has cooled, and bidding wars are less common outside of the most desirable properties and locations.2,4At the same time, prices are not expected to fall meaningfully at the national level. Waiting may result in slightly better selection or marginally lower borrowing costs, but not dramatically cheaper homes.1,3,7 As a result, the advantage in 2026 lies with prepared buyers: those with financing in place, realistic expectations, and flexibility on timing or location.

First-time buyers continue to face the steepest challenges. High upfront costs and qualifying constraints remain barriers, particularly in major metros.14 However, slower price growth and calmer competition give first-time buyers more room to negotiate and plan than during the pandemic surge.9

What This Means for Sellers

For sellers, 2026 is likely to feel more balanced and more demanding than recent years. The automatic leverage sellers enjoyed during the pandemic has faded. Outcomes will depend heavily on pricing accuracy, property condition, and local supply-demand dynamics.7,10Overpricing carries greater risk in a market where buyers are patient and well informed. Homes that are priced correctly and well prepared should still sell efficiently, while those anchored to peak-era expectations may linger.7,10 Concessions and strategic preparation are once again meaningful differentiators rather than optional extras.10

The lock-in effect remains a consideration for homeowners with very low mortgage rates, but life events and accumulated equity increasingly outweigh rate comparisons.11,14 As in the U.S., sellers are slowly recalibrating to the reality that today’s rates are durable, not temporary.

Renters and the Rent-vs-Buy Decision

For renters, 2026 remains a pragmatic decision year rather than a forced transition point. Renting often continues to offer lower short-term costs and flexibility, particularly in high-priced markets.14,15 At the same time, modest price appreciation suggests that waiting indefinitely may not yield better entry points.1,3For those planning to buy in the future, 2026 is best viewed as a preparation window strengthening credit, building savings, and identifying target markets, rather than a year of dramatic opportunity or risk.15

Conclusion: A Market Returning to Rhythm

The 2026 Canadian housing market is defined less by recovery than by normalization. Sales activity is expected to rise modestly. Prices should increase slowly, with wide regional variation. Interest rates are stabilizing rather than collapsing. The extremes of the pandemic era are firmly behind us.Success in 2026 will not come from timing the market perfectly, but from adapting to it. Buyers gain more choice and negotiating room but face ongoing affordability challenges. Sellers retain advantages in undersupplied markets but must price and prepare carefully. Renters balance flexibility against long-term ownership goals.

As the market settles into a more sustainable rhythm, realistic expectations and local expertise matter far more than bold predictions.

Source:

1. Canadian Real Estate Association (CREA).

CREA Updates Resale Housing Market Forecasts for 2025 and 2026.

2. CREA. Quarterly Canadian Housing Market Forecasts.

3. Yahoo Finance Canada. Home prices expected to tick higher in 2026 as sales rebound.

4. Mortgage Professional Canada (MPA). CREA trims 2025 home sales forecast as buyers delay return.

5. CREA. Canadian home sales edge up again following third interest rate cut.

6. CBC News. Canadian home sales rise as buyers slowly return.

7. Royal LePage. Canada’s housing market poised for a reset in 2026.

8. Royal LePage. A reset is in store for Canada’s housing market in 2026.

9. RE/MAX Canada. Canadian Housing Market Outlook.

10. Real Estate Magazine. CREA downgrades housing market forecast.

11. Real Estate Magazine. Five years of market swings set the stage for 2026.

12. Reuters. Bank of Canada seen holding rates as housing stabilizes.

13. Bank of Canada. Monetary Policy Reports & Rate Announcements.

14. Mortgage Professional Canada (MPA). Buyers could edge back to Canada’s housing market in 2026, says Royal LePage.

15. Real Estate Magazine. Real estate trends for 2026: Why Canada’s future may be brighter than it looks.

Planning Your 2026 Real Estate Moves: A Guide to the Best Buying and Selling Seasons [Dec 2025]

Timing isn’t everything in real estate, but it can still be the difference between saving real money or paying a premium, selling in 30 days or sitting for three months, and negotiating from a position of strength or uncertainty. As we look toward 2026, that timing question matters even more in Canada. CREA is calling for a modest pickup in activity into 2026 as rates ease and confidence returns, which means we’re heading back into a more “normal” seasonal market, not the anything-goes conditions of the pandemic years.1 Knowing when to make your move can have a real impact on the outcome.

The challenge? Not everyone gets to wait for the “perfect” month. Job relocations still happen in January. Military, government and corporate transfers often target late spring. Families want to be settled before school starts in September. So instead of chasing a mythical best week, it’s smarter to understand how each Canadian season behaves and then work inside your timeline.

Spring: Peak Selling Season (March–May)

Spring isn’t called peak season by accident. The Canadian market quite literally wakes up after winter. National brokerages like RE/MAX and Royal LePage say the same thing every year: spring is the most desirable time to list because homes simply show better, buyer traffic is higher, and many buyers want to close in time to move over the summer.3,4 A 2024 analysis from Zoocasa looking at several major Canadian markets showed the same pattern, activity typically ramps up in March, peaks through April and May, and in some years even starts a touch earlier as buyers try to get ahead of the spring rush.2

Buyer psychology helps. Longer daylight means more evening showings. Melting snow and fresh landscaping make detached homes look their best. And families with school aged kids start shopping in March and April so they can move in July or August. In years when inventory is tight in Toronto, Vancouver, Ottawa/Gatineau or Victoria, this spring surge can still create multiple-offer situations especially on well-priced, well-located properties. That will be even more likely if 2025’s softer prices tempt more buyers back in 2026.

The Competition Factor

Of course, spring’s upside comes with a trade-off: everyone else knows it’s a good time too. More listings hit the market, so sellers have to do the basics well accurate pricing, strong photos, pre-list prep, and real marketing to stand out. Buyers benefit from more choice, but they also face the most competition for the “nice” listings. In hot pockets of the GTA, Calgary, Halifax or parts of the Lower Mainland, that can still mean acting quickly and writing tighter offers than you would in October.

Summer: Extended Peak Season (June–August)

As spring rolls into summer, the Canadian market usually keeps much of its momentum. June is often one of the busiest closing months of the year, and in Quebec there’s an extra push because so many leases turn over on or around July 1 “moving day” which keeps trucks, buyers, and sellers active.6

Summer lines up perfectly with family life. Kids are out of school, weather is predictable, cottages are opening, and people have time to tour. Outdoor features also show at their absolute best decks, patios, rooftop terraces, west-facing balconies in Vancouver, even small yards in Toronto. Buyers will often pay a convenience premium here because moving in July is simply easier than moving in January.

By late August, however, you can feel things shift. Early-summer listings that were too ambitious on price can start to look “stale.” Families are turning their attention back to school. Serious buyers are still around, but urgency eases good news if you were beaten out in June.

A Note on Moving Costs

There’s a very Canadian practical piece people forget: it literally costs more and is harder to book a move in peak season. In Quebec, July 1 is so busy that moving companies advise booking months in advance, and local news outlets report higher rates around that date because demand is intense.6 If your timing is flexible, a late-fall or winter move can save you money.

Fall: Underrated Opportunity Season (September–November)

Fall might be real estate’s best-kept secret on both sides of the transaction. After summer vacations, a lot of qualified buyers come back into the market, but there are usually fewer new listings than in April or May. That combination gives good properties room to stand out. Royal LePage and Global News have both been noting that fall 2025 is showing more balance and a bit more negotiating room, and if that pattern continues, fall 2026 could be an excellent time for buyers who want value without spring’s bidding wars.4,5

For sellers, fall has another quiet advantage: buyers are more serious. Casual browsers drop off once school resumes and weather cools. People shopping in October usually want to be in before snow and holidays. That natural year-end urgency close before winter, avoid carrying costs over the holidays, move before the deep freeze helps deals get done.

This is also when price gaps from summer can show up. As activity cools and more listings sit, buyers can sometimes negotiate a bit more, especially in markets where 2025 softness hasn’t fully cleared out by early 2026. You may not see a giant discount in downtown Toronto or central Vancouver, but you can often get better terms.

Winter: Value Season (December–February)

Winter gets a bad reputation in Canadian real estate because showings are harder, curb appeal is lower, and nobody loves moving in slush. But for buyers with flexibility, winter is often the best value play of the year. Fewer people list when it’s -15°C, so the buyers who are out have more leverage days on market are longer, and sellers who have to sell are more negotiable. CREA’s 2025 numbers already show a market that’s sensitive to confidence and rates; if that softer tone spills into early 2026, winter buyers will be in a good position.1

Winter also tells you the truth about a property. You can see how the home actually handles a Canadian winter drafts, windows, ice dams, heating information you can’t always get from a May showing. That’s powerful for inspections and negotiations.

There are trade-offs, of course. Sellers face the lowest foot traffic of the year, holiday distractions, and limited daylight for showings. Curb appeal is just harder when everything is under snow. But fewer competing listings can work in your favour if you price realistically and present well. Serious buyers will still come out in January especially job relocations.

Regional Differences: Not All Canadian Markets Are Equal

One thing we have to say in a Canadian version of this post: where you live matters a lot. Seasonal swings are sharpest in places with real winters and short construction/moving seasons think the Prairies, Atlantic Canada, and most of Quebec because everyone tries to cram listing, selling, and moving into a six or seven month window. In those places, spring and summer really do carry most of the year’s volume.

In contrast, the BC Lower Mainland and much of Southern Ontario can support more year-round activity because weather is milder and buyers stay engaged. Those markets can have excellent fall seasons, and even winter sales don’t fall off a cliff the way they do in January in Winnipeg.